PPF account turns dormant if you invest less than ₹500 a year: What you lose and how to revive it

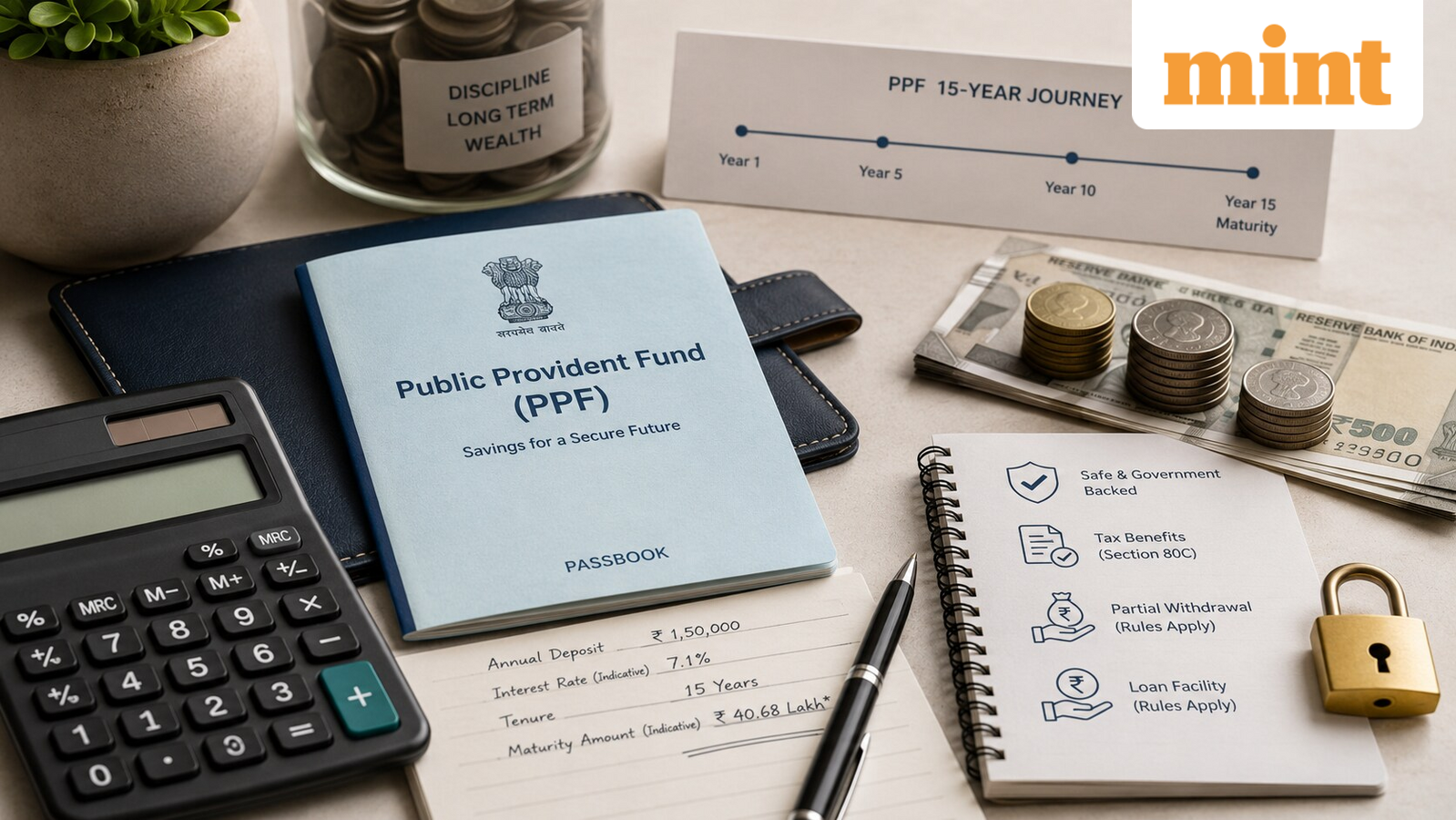

Public Provident Fund (PPF) is a long-term savings scheme with a 15-year lock-in period and attractive features such as tax advantages on investments, interest earnings, maturity proceeds, and a decent interest rate of 7.1% per annum. However, account holders are required to make at least one contribution every financial year to keep the account active.

Many investors may be unaware that failing to deposit the minimum required amount of ₹500 in a year can make the account inactive, restricting further deposits and access to all the above mentioned account benefits. If your PPF account has lapsed due to non-compliance, it can be reactivated by following a simple prescribed process.

What you lose if your PPF account becomes inactive?

An inactive PPF account continues to earn interest on the existing balance but the account gets restricted, meaning you won’t allowed to perform certain tasks against it unless you reactivate it.

No fresh deposits can be made while your account remains inactive which makes you miss out on earning interest on additional contributions and lose the long-term benefit of compounding that regular investments would have generated.

Account holders are also not allowed to get loans against the PPF balance or make partial withdrawals during this period.

Although the account continues to earn interest and matures after the prescribed 15-year tenure, access to certain account facilities remains restricted unless the account is revived, according to a Paisabazaar report.

How to reactivate your lapsed PPF account?

Reactivating an inactive PPF account is feasible, but specific steps must be followed along with the payment of a penalty. Follow the steps provided below to reactivate your PPF account:

- Go to the branch from where you operate your PPF account, whether it’s a bank or a post office.

- Submit a written request for reactivation, clearly stating your intent to revive the account.

- Pay the penalty amount ( ₹50 for every year of inactivity)

- Deposit the minimum subscription amount required for the ongoing financial year, which currently stands at ₹500.

The reinstated account will resume earning interest from the date of reactivation and to ensure that it does not lapse again, investors should uphold the minimum annual contribution of ₹500 after reactivating the account.

Who can open a PPF account and features

Any resident Indian individual can open a PPF account. Additionally, parents or legal guardians can open a PPF account on behalf of a minor child.

Like we discussed, investors must deposit at least ₹500 in a financial year to keep a PPF account active. The maximum amount that can be invested across all PPF accounts in a year is capped at ₹1.5 lakh.

A PPF account matures after 15 complete financial years from the end of the financial year in which it was opened. Upon maturity, investors can extend the account in blocks of five years as many times as they want.

Though PPF comes with a 15-year lock-in period, investors can make partial withdrawals from the 7th financial year onward. Premature closure is allowed only after five years under certain circumstances such as higher education or serious medical treatment, but a 1% penalty on interest rate will be applicable for such withdrawals.

PPF also offers tax benefits under the EEE (Exempt-Exempt-Exempt) regime, meaning you can save taxes at three distinct stages: investment, interest accrual, and maturity, which makes it a popular savings scheme for long-term and conservative investors.